Apple Stock Analysis

Stock of the Month | November 2025

8 min

Executive Summary

- Q4 Performance: $102.5B revenue (+8% YoY); Services hit record $108.6B annually (26% of revenue, ~50% of profits)

- Cash Generation: $98.8B free cash flow with $110B+ returned annually via dividends and buybacks (40% share count reduction)

- Valuation: Trading at 30x P/E; DCF models suggest 15-27% premium to intrinsic value

- Catalysts: Apple Intelligence rollout, iPhone 17 upgrade cycle, holiday sales momentum

- Risks: Regulatory pressure (EU/UK), tariff costs ($800M-$1.1B quarterly), competitive AI positioning

What Apple Does

Apple designs and manufactures consumer electronics (iPhone, iPad, Mac, wearables) plus a growing services business (App Store, iCloud, Apple Pay, AppleCare). The ecosystem creates powerful lock-in effects.

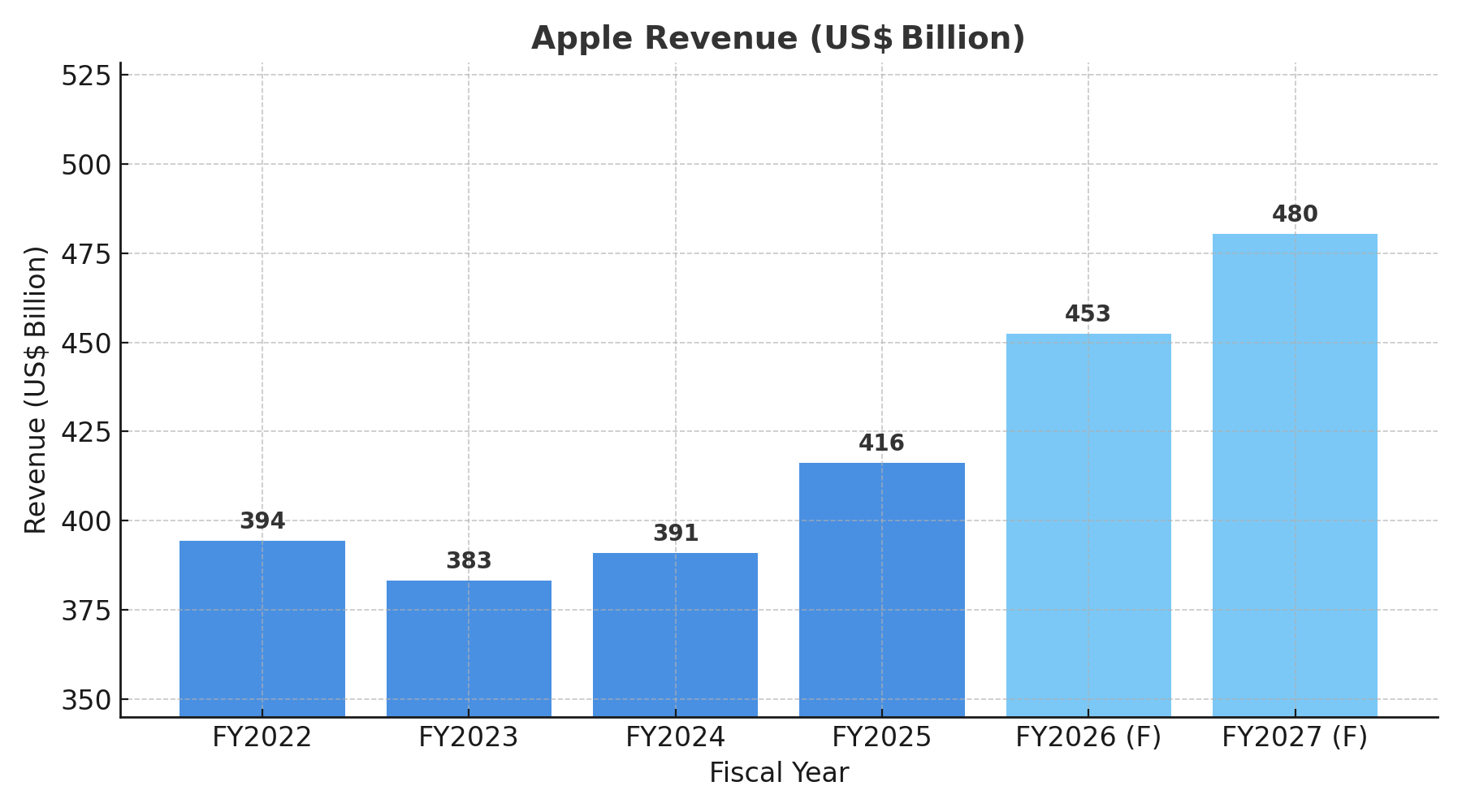

FY2025: $416B revenue • Q4: $102.5B (+8% YoY) • Services: $108.6B (record high)

5-Year Share Price Performance

💰 Apple's Revenue Breakdown

| Product Category | Revenue | % of Total |

|---|---|---|

iPhone Flagship product line |

$208B | 50% |

Services 🔥 App Store, iCloud, Apple Pay, etc. |

$108.6B | 26% |

Mac MacBook, iMac, Mac Studio |

$37.4B | 9% |

iPad iPad Pro, iPad Air, iPad Mini |

$33.3B | 8% |

Wearables & Accessories AirPods, Apple Watch, HomePod |

$28.7B | 7% |

Free Cash Flow Projection & Valuation

Apple's cash generation machine continues its strong trajectory, with Free Cash Flow (FCF) expected to grow significantly through 2028 as services scale and operational efficiency improves.

| Fiscal Year | Free Cash Flow | YoY Growth |

|---|---|---|

| FY2022 | $111.4B | — |

| FY2023 | $99.6B | -10.6% |

| FY2024 | $108.8B | +9.2% |

| FY2025 | $98.8B | -9.2% |

| FY2026E | $127.6B | +29.2% |

| FY2027E | $138.0B | +8.2% |

| FY2028E | $154.7B | +12.1% |

🔍 Discounted Cash Flow (DCF) Analysis

Multiple DCF models from reputable sources suggest Apple's current share price of $275.41 trades 15–27% above calculated intrinsic value, depending on growth and discount rate assumptions. This reflects investor optimism about AI monetization and services expansion but signals limited margin of safety at current levels.

| Scenario | Fair Value | vs. Current |

|---|---|---|

| Bear Case | $196.54 | -27% |

| Base Case | $220.39 | -20% |

| Bull Case | $263.30 | -4% |

Standard DCF Assumptions (10-Year Model)

• Starting FCF: $97–110B

• WACC: 9–10%

• FCF Growth: 4–6% annually

• Terminal Growth: 2.5–3%

The Investment Case

Apple's investment thesis balances significant growth opportunities against notable headwinds. While the company's ecosystem strength and innovation pipeline provide resilience, investors must weigh regulatory challenges and valuation premiums.

🚀 Growth Tailwinds

- AI Integration: Apple Intelligence features drive iPhone upgrades and create new revenue streams

- Services Growth: High-margin recurring revenue (App Store, iCloud, subscriptions) now 26% of total sales

- Ecosystem Lock-In: 2B+ active devices create powerful customer retention and cross-selling opportunities

- Capital Returns: $110B+ annually via buybacks and dividends reduces shares outstanding, boosting per-share earnings

⚠️ Key Risks

- Regulatory & Tariff Headwinds: Facing antitrust investigations in Europe over App Store practices, while new trade tariffs add $800M-$1.1B in quarterly costs

- AI Competition: Apple entered the AI race later than competitors like Google and Microsoft, potentially limiting market share in emerging AI applications

- Premium Valuation: At 30x earnings, the stock price already reflects high expectations—leaving little room for error if growth disappoints

The Bottom Line

Strong Q4 performance driven by services (now 25% of revenue, ~50% of profits). Apple returns $110B+ annually to shareholders through dividends and aggressive buybacks, reducing share count 40% over the past decade.

Key catalysts: holiday sales, Apple Intelligence adoption, services momentum. Main risks: regulatory pressure, tariff costs ($800M-$1.1B quarterly), and competitive AI positioning.